You can know. See how much you can confidently spend, and how to keep more of it, on the most conservative market on record.

A spreadsheet, even a good one, gets these wrong. Lumifin runs all six and hands you one number: what you end with.

Cross the ACA cliff by one dollar and you lose $10,000 to $20,000 in subsidies that year. Lumifin keeps your income under the line.

Federal, capital gains, and IRMAA brackets shift year by year. Guess wrong once and the bill compounds. Lumifin shows the real number for every year.

Draw from the wrong account first and you pay taxes you never owed. Lumifin finds the order that keeps more.

Convert too much and you spike your bracket. Too little and RMDs get you later. Lumifin sizes conversions to your bracket, not a rule of thumb.

Claim at the wrong age and you lock in a smaller check for life. Lumifin fits the claiming age to your full withdrawal plan.

At 73 or 75 the IRS forces withdrawals whether you need the money or not. Lumifin eases the tax hit before it lands.

Real screens from the app. Click through all five steps.

Start with what's actually true for you: your accounts, income, and spending. Every assumption stays yours to change.

Not just your accounts and income. The engine factors in taxes (federal and state), healthcare, market swings, and life events.

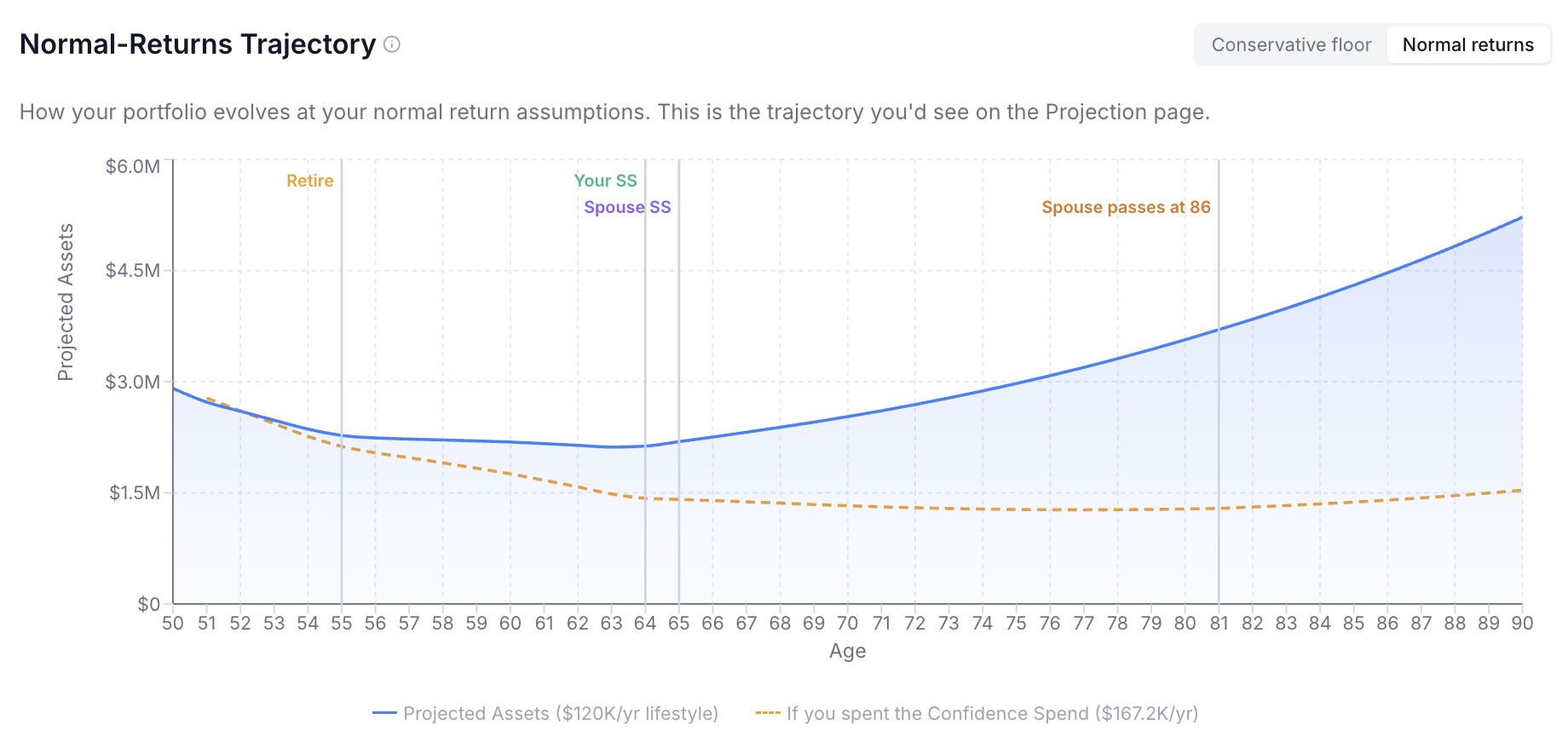

Run to your end age at normal return assumptions. This is the trajectory the Projection page shows.

The detail behind your projection

Traditional, Roth, and taxable tracked separately, because each is taxed differently.

Salary, rental, pension, part-time, and Social Security, each layered into the right bracket.

Every number in today's dollars, so you compare like for like across the years.

Cost basis tracked, with long-term, short-term, and qualified rates applied.

Both spouses' accounts and benefits, including what happens when one passes.

ACA subsidy cliffs before 65, Medicare premium surcharges (IRMAA) after. Both swing with the income your withdrawals create.

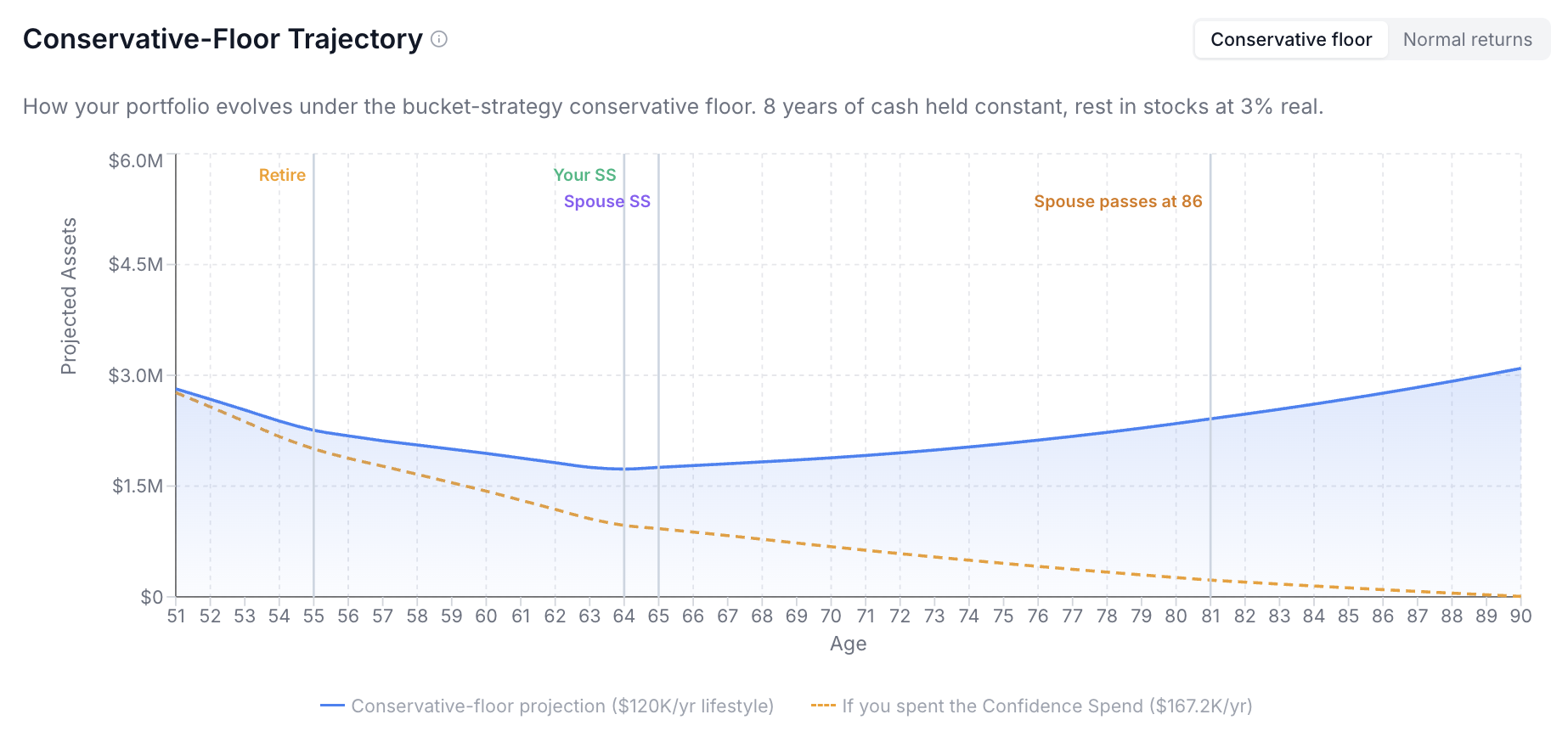

Your after-tax number, planned against the worst market on record.

Your Confidence Spend is built on the worst 30-year market on record: 8 years of cash, the rest in stocks. This is the floor your money holds to.

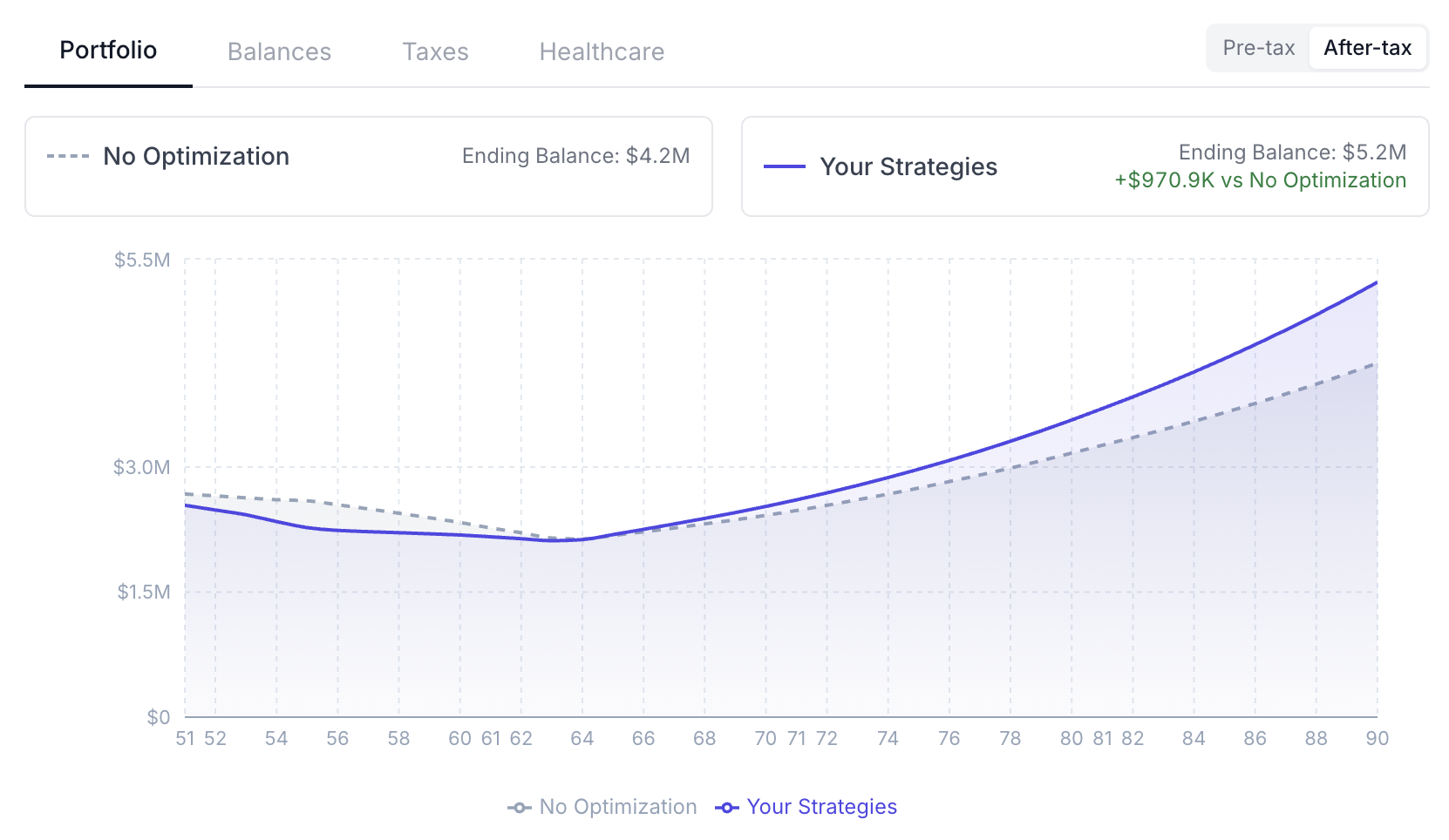

The right contributions, withdrawal order, and Roth conversions can leave you with hundreds of thousands more by your end age: same portfolio, same spending, just a smarter plan.

The same portfolio under two plans, tracked to 90: do nothing vs. your optimized withdrawals and conversions. The gap between the lines is what the strategy is worth.

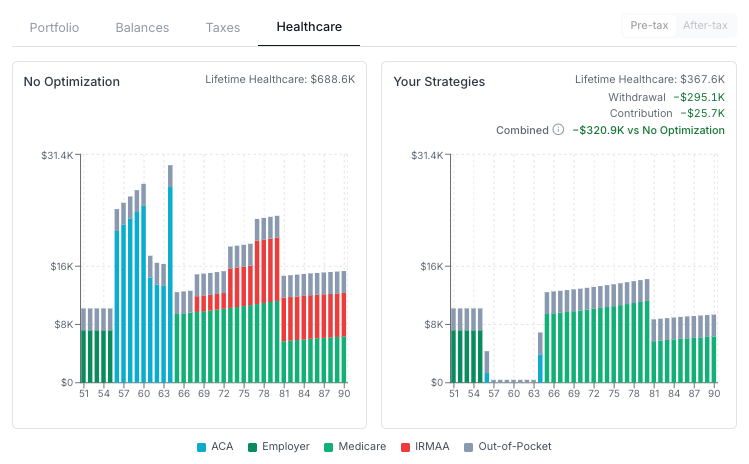

Lifetime healthcare before and after: ACA premiums in the gap years, then Medicare and IRMAA. Holding your income under the cliffs cuts the total, year by year.

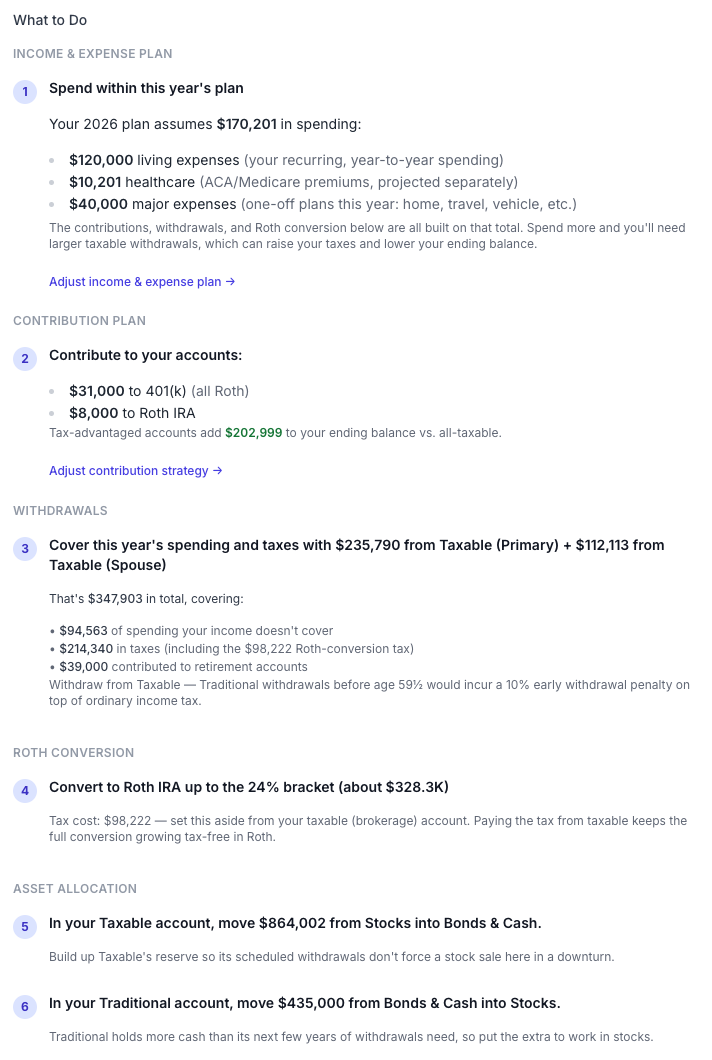

Not just "you're on track": every move in your plan, spelled out for the year ahead and refreshed each year as life changes, so you can confidently spend your time and money on what matters most.

See how much you can confidently spend, then keep more of it. Model as many scenarios as you want.

Full Lumifin app access for a year: model your own retirement decisions, scenario by scenario.

Want to see it first? Book a 20-minute discovery call →

Now: Join the waitlist free: your name, email, and three quick questions about your situation.

August 2026: The intake opens: 30 spots, hard cap. Invitations go out in waitlist order; you claim yours at $199/yr and your access starts the same day.

Guarantee: 30-day money-back guarantee from the day you pay: payment and access start together.

Each calculator answers one piece of the picture. The full app above puts them together into a single year-by-year plan.

See how much you can safely spend (and how long your money lasts) stress-tested against the worst 30-year market on record.

Calculate your number →Retiring before 65? See what health insurance will really cost in the gap years, and where the subsidy cliff bites.

Check your subsidy →See your projected RMD tax bracket, and whether converting now (and how you pay the tax) leaves you with more.

Plan your conversion →Want to see it first? Book a 20-minute discovery call →