If you think you'll pay 22% or 24% on your retirement withdrawals, you're probably overestimating by two to three times.

I hear it constantly: "I'll be in the 22% bracket, so I'll lose a quarter of every withdrawal." That is not how it works, and the gap between what people expect and what they actually pay is enormous.

Your real retirement tax bill comes down to three things:

- Which accounts you withdraw from. Traditional, Roth, and a regular brokerage account are taxed three completely different ways.

- How much you pull out in a year. The bracket system rewards you for staying in the lower bands.

- What state you live in. Washington takes nothing. California can take 9% or more on top of federal.

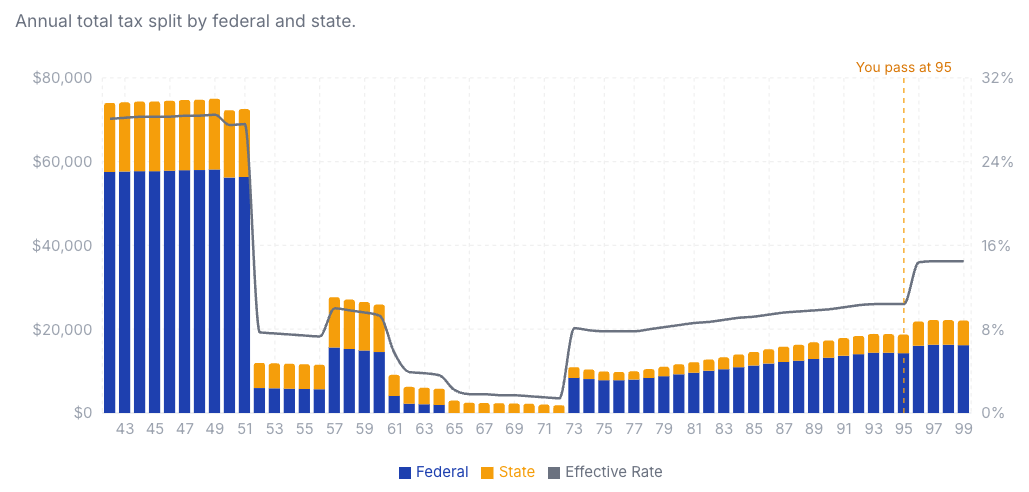

The worst case: everything in a Traditional 401(k)

Start with the least tax-friendly setup: a married couple with all of their money in a Traditional 401(k), where every dollar withdrawn counts as ordinary income.

| Annual withdrawal | Washington | California |

|---|---|---|

| $80K | 6.7% | 8.6% |

| $120K | 8.5% | 11.5% |

| $200K | 13.4% | 18.8% |

Even pulling $200K out in California, a high-tax state with no Roth or brokerage cushion, the effective rate is about 19%. Not 22%, not 24%.

Now spread the money across account types

Watch what happens when the same $120K withdrawal comes from a mix instead of one bucket: $60K from the Traditional 401(k), $36K from a brokerage account, and $24K from a Roth.

- Washington: about 2.5%

- California: about 3.7%

Held longer than a year, the brokerage piece is mostly your original cost basis (no tax) plus long-term capital gains, which are taxed at a lower rate than ordinary income. At this income level the federal long-term capital gains rate is 0%. The Roth piece is tax-free entirely. Stacking the three accounts deliberately can cut your effective rate by 70% or more.

And if everything is in a Roth? Zero percent, in either state.

Why people get this so wrong

Two reasons.

First, they confuse the marginal bracket with the effective rate. The 22% is the rate on your last dollar, not your average. The system is progressive: your first dollars are taxed at 10%, the next at 12%, then 22%. Your actual tax is the average across every dollar.

Second, they forget the standard deduction. For a married couple it shields roughly the first $32.3K entirely, before any bracket applies.

Why your number matters

Knowing your real retirement tax rate isn't trivia. It is the first input to the biggest decisions you'll make: how much you can safely spend each year, when you can afford to stop working, and whether to convert to Roth in the years before required withdrawals begin.

If you've been mentally penciling in 22 to 24%, you're likely planning around a number that is two to three times too high. That pessimism can keep you working longer than you need to, or spending less than you've earned.

One important caveat: the examples above use the standard withdrawal order (taxable first, Traditional second, Roth last). That is a common rule of thumb, not an optimized plan. With strategic Roth conversions in your lower-income years, the required-withdrawal tax wall later in retirement can shrink, and your ending balance can grow meaningfully. That's a deeper topic for another post.

Numbers based on 2026 federal and California rates, married filing jointly, standard deduction only. They exclude Social Security taxation, IRMAA, and other income sources, which layer on top. Brackets and rates change over time. Educational only, not financial or tax advice. Model your own numbers, or check with a fiduciary advisor or CPA, before acting.