Updated June 12, 2026: we found and fixed a bug in our projection engine that overstated this post's original figures. The example below has been re-run on the corrected engine. The headline numbers changed, and so did the winning strategy. The lesson got stronger, not weaker.

What is a "withdrawal strategy," and should you care?

It is the plan for how you fund retirement from your portfolio: how much you pull each year, and from which account type. And the account you tap changes your tax bill, which ripples into how the rest of your money grows.

Three account types, taxed three ways

- Taxable (a regular brokerage account): you owe capital gains tax when you sell, plus tax on interest and dividends along the way, which slows the growth.

- Tax-Deferred (401(k), traditional IRA): every dollar you take out is ordinary income.

- Tax-Free (Roth): nothing is taxed coming out.

Pull the same amount from different accounts and your tax bill can look completely different. That is the whole game.

A real example

Take a 41-year-old couple with a $2.8M portfolio, $500K of it tax-deferred, still working.

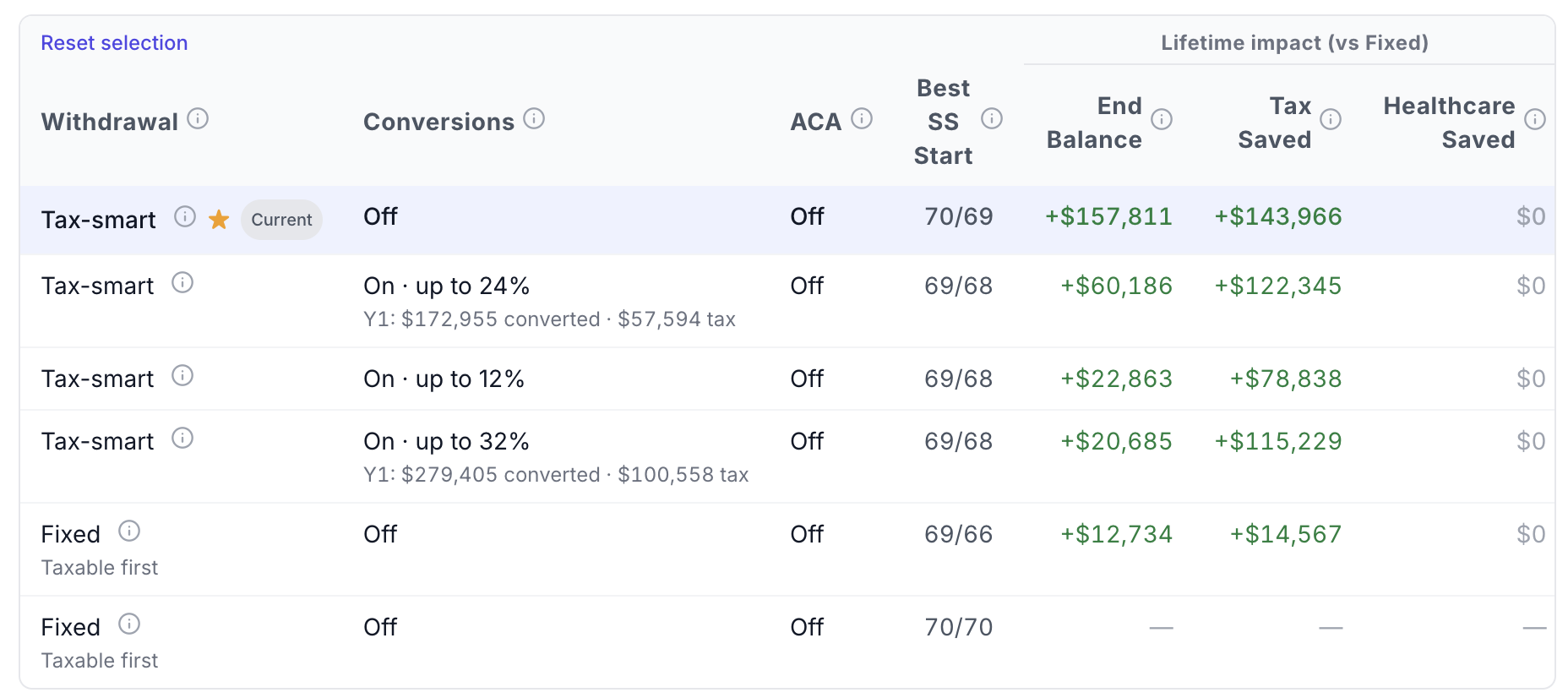

Run their accounts through every combination of withdrawal order, Roth-conversion ceiling, and Social Security claiming age, and the plan that comes out on top is not the one most people would guess: a tax-smart withdrawal order (Lumifin picks which account to tap each year based on your tax brackets), Social Security delayed to 70 (69 for the spouse), and Roth conversions left off.

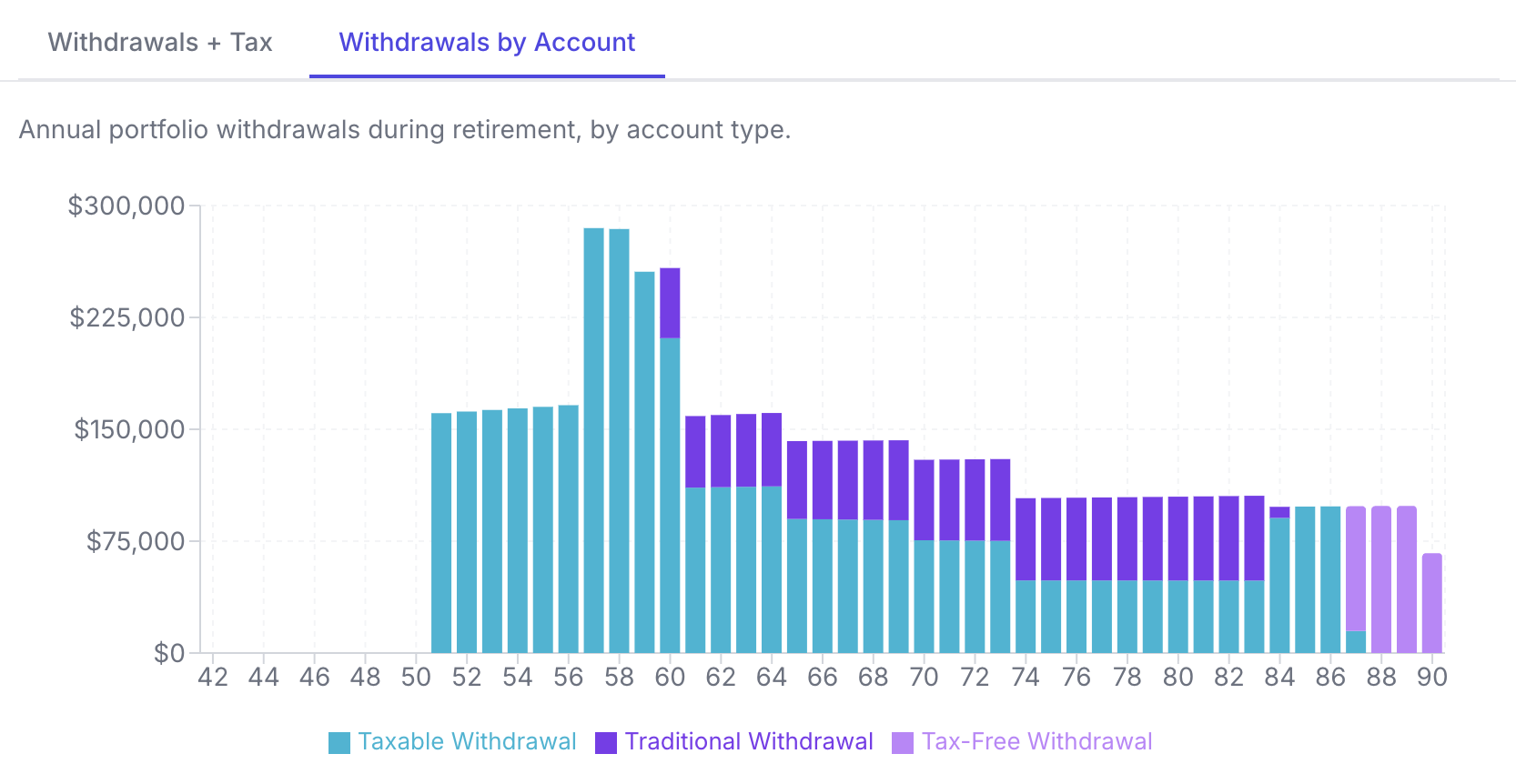

And here is what that order actually looks like, year by year. Taxable covers the early retirement years. Traditional withdrawals layer in from the late 50s, sized each year to fill the lowest tax brackets first (the slice under the standard deduction comes out at 0% tax). The Roth is barely touched until the very end, where its tax-free dollars stretch the portfolio's final years.

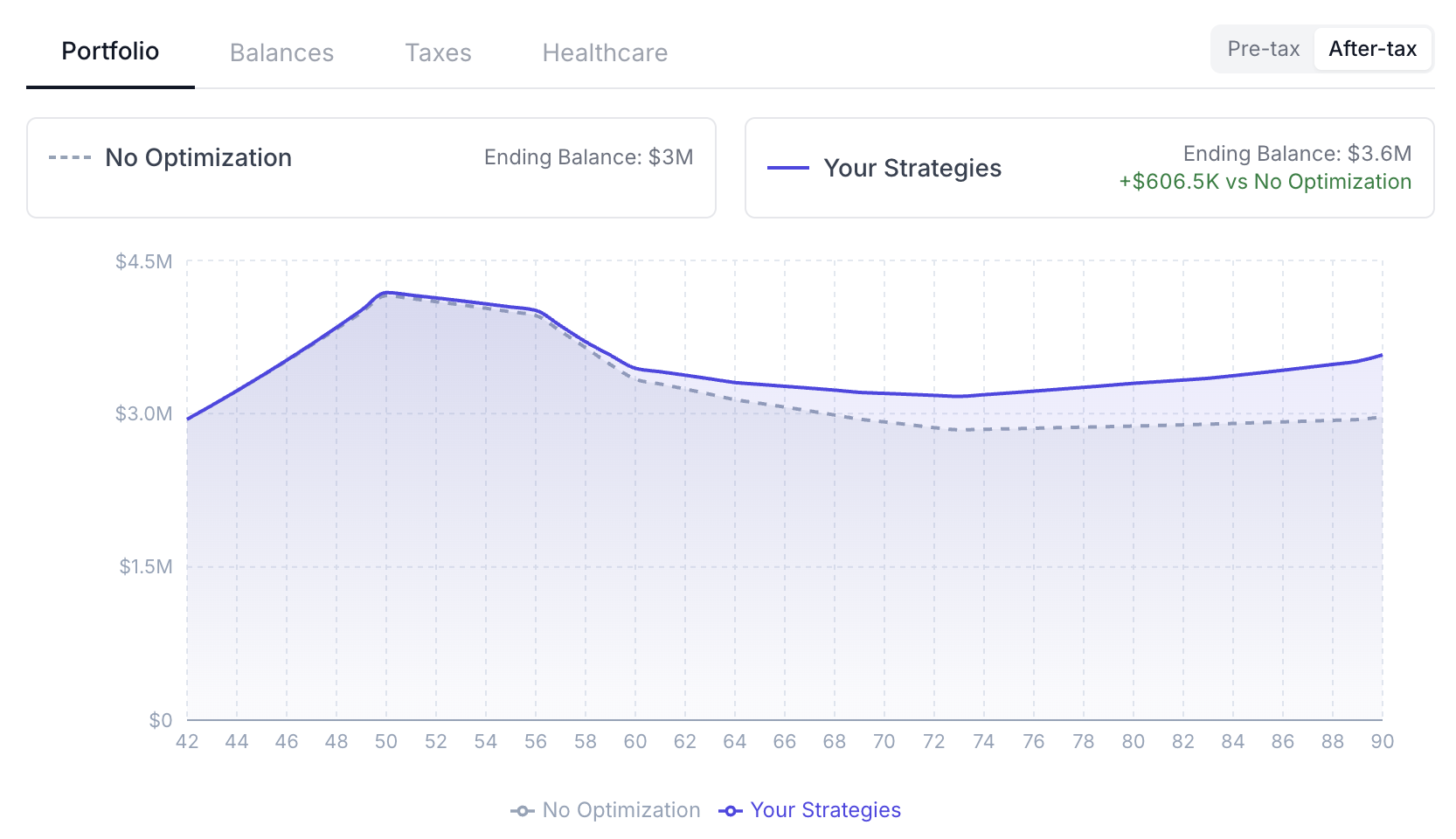

Versus doing nothing (the default fixed order, no optimization at all), that plan is worth roughly:

- $606.5K more in after-tax value at age 90

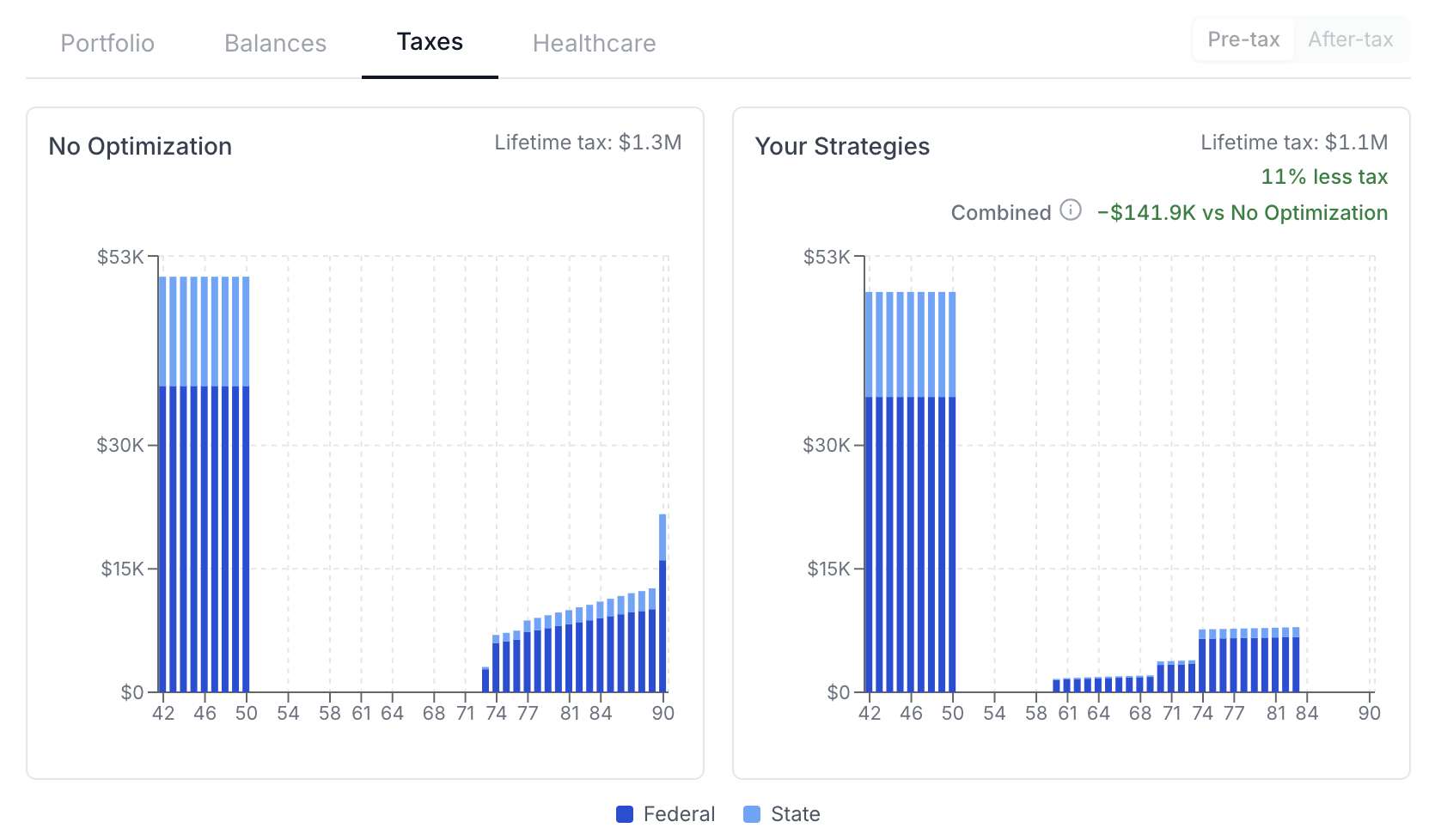

- $141.9K less in lifetime taxes, about 11% (from $1.3M down to $1.1M)

And here is the counter-intuitive part: Roth conversions did not make the cut. The variant everyone asks about first, converting up to the top of the 24% bracket, ends about $98K behind the no-conversion plan in this scenario ($60,186 vs $157,811 ahead of the fixed taxable-first order). With only $500K of the $2.8M in tax-deferred accounts and two salaries still coming in, conversions would prepay tax at a higher rate than those dollars are likely to ever face later. For this couple, the leverage is in which account they tap first and when they claim Social Security, not in conversions.

That is exactly why you model instead of guess. The "obvious" lever lost, and two quieter levers won.

Model it, don't guess

Here is the gap I keep running into. Most planning tools are excellent at modeling a strategy you choose: you set the conversion ceiling, the withdrawal order, and the Social Security age, and the tool shows you the tax consequences. What they rarely do is search across all of those levers at once to find the best combination, with the ACA and IRMAA cliffs built in as constraints rather than footnotes.

And those levers interact. Social Security taxation eats into your bracket room. IRMAA tiers step up at income thresholds. Before 65, the ACA subsidy cliff changes the math entirely. The optimal combination moves when you account for all of them together, one lever at a time isn't enough.

If you're planning your own retirement, the lesson is simple: the order you withdraw in, when you claim, and whether you convert at all, is worth real money. It's worth modeling before you're living off the portfolio, not after.

Example figures come from a single modeled scenario (41-year-old couple, $2.8M portfolio, $500K tax-deferred, planning to age 90), re-run on the corrected engine on June 12, 2026, and are specific to its assumptions. Educational only, not financial or tax advice. Everyone's situation is different. Model your own numbers, or check with a fiduciary advisor or CPA, before acting.